The COVID-19 pandemic that swept through the world in 2020 – and is still not over – had a high toll on human life, social and economic wellbeing. Supply chains were interrupted, schools and shops closed, office workers turned their homes into makeshift offices, air traffic came to a near standstill. The combined GDP of the G20 combined fell by 3% in 2020 but rebounded by 6.1% in 2021.

Not surprisingly, it has its effect on emissions as well – as a sufficient decoupling of emissions from economic activity has not happened yet. According to the Climate Transparency Report 2022, published on 20 October, total energy-related CO2 emissions dropped by 4.9% in 2020 only to increase again by 5.9% in 2021.

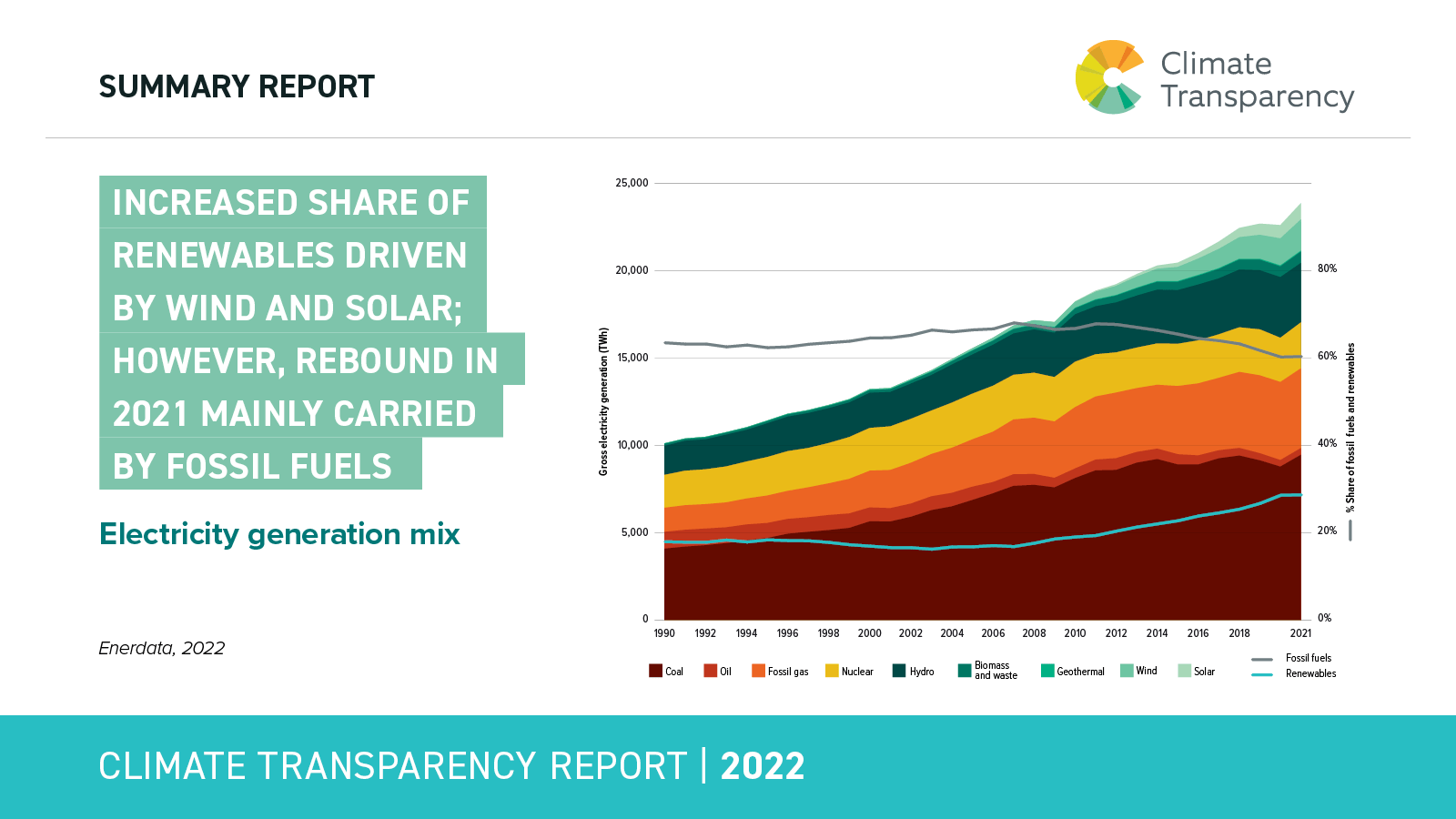

This rebound can be observed also on a sectoral level. For example, power sector is responsible for 40% of the energy-related CO2 emissions in the G20 in order to generate electricity. Electricity use is expected to grow worldwide every year, both to provide energy to the nearly one billion people without access to electricity, and to electrify transport, buildings and industry. Emissions from electricity generations have jumped by 7.1% in 2021 after a decrease of 2.8% the year before. Per capita, emissions reduced by 3% between 2015 and 2019.

Yet, the strong increase of emissions demonstrates that renewables – though they have been expanded significantly over the last ten years – have not grown strong enough to balance the increase in electricity consumption. The increase of renewable energy in the power mix, in the last years has been mainly driven by wind and solar. However, the economic recovery in 2021 was mainly carried by fossil fuels leading to this strong rebound of emissions. The upward trend for share of renewables in the power sector slowed down during the pandemic, staying at 28% of the power mix in 2020 and 2021. At the same time, the downward trend of fossils also slowed down, staying at 60% of the electricity generation mix in 2020 and 2021.

Other than the power sector, per capita emissions in the transport sector had grown by 6% between 2015 and 2019. They also fell sharply in 2020 by 11.5% – only to climb back up in 2021 by 7.7%. In China and Turkey, they even exceeded pre-pandemic levels.

It seems possible that business travel by air, which was expected to experience above average growth rates, might not grow strongly or at all as many companies and employees have experience the lower cost and time saving of online meetings. Whether this is a structural behavioural shift is not yet clear. Indications in 2022 show, however, that on average, mobility will increase further to above pre-pandemic levels.

What does this tell us for the general emissions trends – will the rebound be limited, and emissions stay on the plateau we have seen in 2018?

According to a recent forecast by the International Energy Agency that global CO2 emissions from fossil fuel combustion are expected to grow by just under 1% in 2022 as a strong expansion of renewables and electric vehicles prevents a much sharper rise (Link). Yet, we are beyond the time when one could take the near plateauing of emissions as a positive sign. According to the UNFCCC 2022 Nationally Determined Contributions Synthesis Report (Link), the combined climate pledges of 193 Parties under the Paris Agreement could put the world on track for around 2.5 degrees Celsius of warming by the end of the century – this is far from the long term temperature goal of the Paris Agreement.