The rebound of emissions in 2021 from a temporary dip in 2020 by 5.9%, induced by the COVID-19 pandemic, is in stark contrast to initial hopes for environmentally and socially sustainable solutions at the heart of economic recovery packages. The G20 spent more than 14 trillion USD on various economic stimulus packages during the COVID-19 pandemic. Only two per cent, or about 300 billion USD, was directed to the much-heralded ‘green’ recovery.

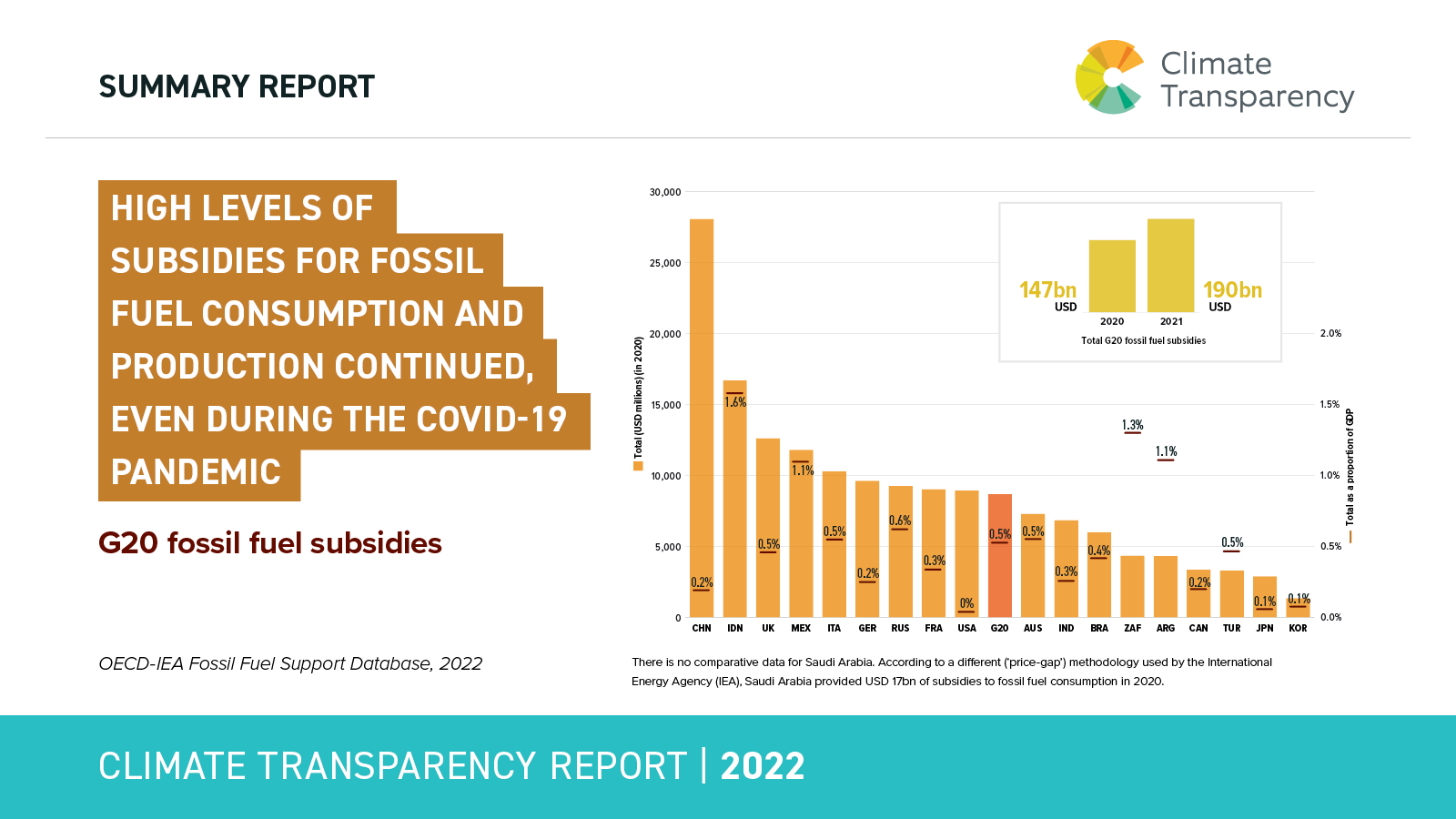

At the same time, the G20 has continued to show largesse to the fossil fuel industry. The subsidy figures show that G20 governments did not fully commit to a greening of the economy, especially the energy sector, but actually further strengthened the fossil fuel industry domestically and abroad. A longstanding G20 commitment first issued in 2009 to phase out fossil fuel subsidies is conveniently and repeatedly forgotten. The confirmation of the Paris Agreement to limit temperature increase to 1.5°C by 2022 G20 Bali Leaders Declaration under the Indonesian Presidency lack action.

To name an example from Climate Transparency’s Country Profile on Germany: By far the largest energy-related financial measure by Germany in 2021 was to give an export credit guarantee (Euler Hermes Bürgschaft) to Russia’s state-owned energy group, Gazprom: 2.9 billion USD to develop the Amur Gas Processing Plant.

In 2020 governments of the G20 poured at least USD 147 billion USD in subsidies into the industry that is most harmful for the climate only to increase it to 190 billion USD in 2021. In total, the G20 have committed in 2020-2021 to at least USD 1.10 trillion to supporting different energy types through new or amended policies. The of that sum had no ‘green strings’ attached. It is therefore no surprise that with increased economic activity, emissions went up again. Both the G20’s Gross Domestic Product and total emissions grew in 2021. The sufficient decoupling of emissions from growth that is urgently needed if emissions to be kept below dangerous levels still did not happen.

By the end of 2021, the previously very low prices for fossil fuels were starting to rise again, reaching pre-pandemic levels. The G20 seemed set to return on their pre-pandemic pathway – no way near the ambitious high road needed to keep global temperatures below the 1.5°C mark.

Then, Russia invaded Ukraine on February 24, 2022, and the global energy market changed profoundly. Russia’s war on Ukraine has had a resounding effect on energy prices, availability, and security. Europe is searching for sellers of gas in order to compensate a severe downturn of gas imports from Russia. The price for gas in Europe in consequence in autumn 2022 has been about 3 times higher than in the beginning of 2022. Throughout the G20 in 2022, prices for fossil fuels have increased to varying degrees – be it an increase of 130% for liquefied gas in Japan, or 170% for South African coal. This has severe implication for energy prices and security in developing countries. For example, Pakistan faces a severe shortage of LNG in the coming winter.

Governments have reacted with a number of ‘ad hoc’ quick policy fixes in order to guarantee energy security and to keep prices for (fossil) energy affordable for people, business, and industry. There has been a large variety of these measures – be they price caps on gas in France, reimbursement schemes in Germany, or reduced petrol taxes in Japan. Many other countries of the G20 have implemented similar measures. These measures are certainly no good news for the achievement of countries’ nationally determined contributions. It remains to be seen how long they will stick around – the longer, the worse for the climate.

The world’s energy systems are at a crossroads, and policy makers of G20 countries have a choice to make if they take the ‘high road’, or the ‘low road’. Against the background of the weak results of the COP28, G20 governments are responsible to make the difference, and follow their commitment to 1.5°C in the Bali Leaders Declaration.

The ‘low road’ would satisfy the short-term demands of citizens and industries to ensure safe and continued access to fossil fuels on a low-ambition, high-emissions pathway. This would lead to continued high investments in fossil fuel infrastructure and exploration, to maintain business-as-usual. Cost of fossil fuels will likely fall (and already has), but not to pre-pandemic levels, so exploration of fossil fuel deposits will continue to be economically attractive. The resulting path will lock in emissions for many decades, at the expense of catastrophic global climate change.

The ‘high road’ on the other hand would satisfy the need for energy security beyond short-term economic interests on a high-ambition, low-emissions pathway. The high road would entail that governments increase the price of carbon to reflect its true environmental and social cost, a strong focus on energy conservation, and expand renewable energy to a level where fossil fuels do not play a significant role in the energy mix. The resulting pathway will keep emissions down, ensure safe access to energy at reasonable costs, at the expense of a number of incumbent industries in a few countries.

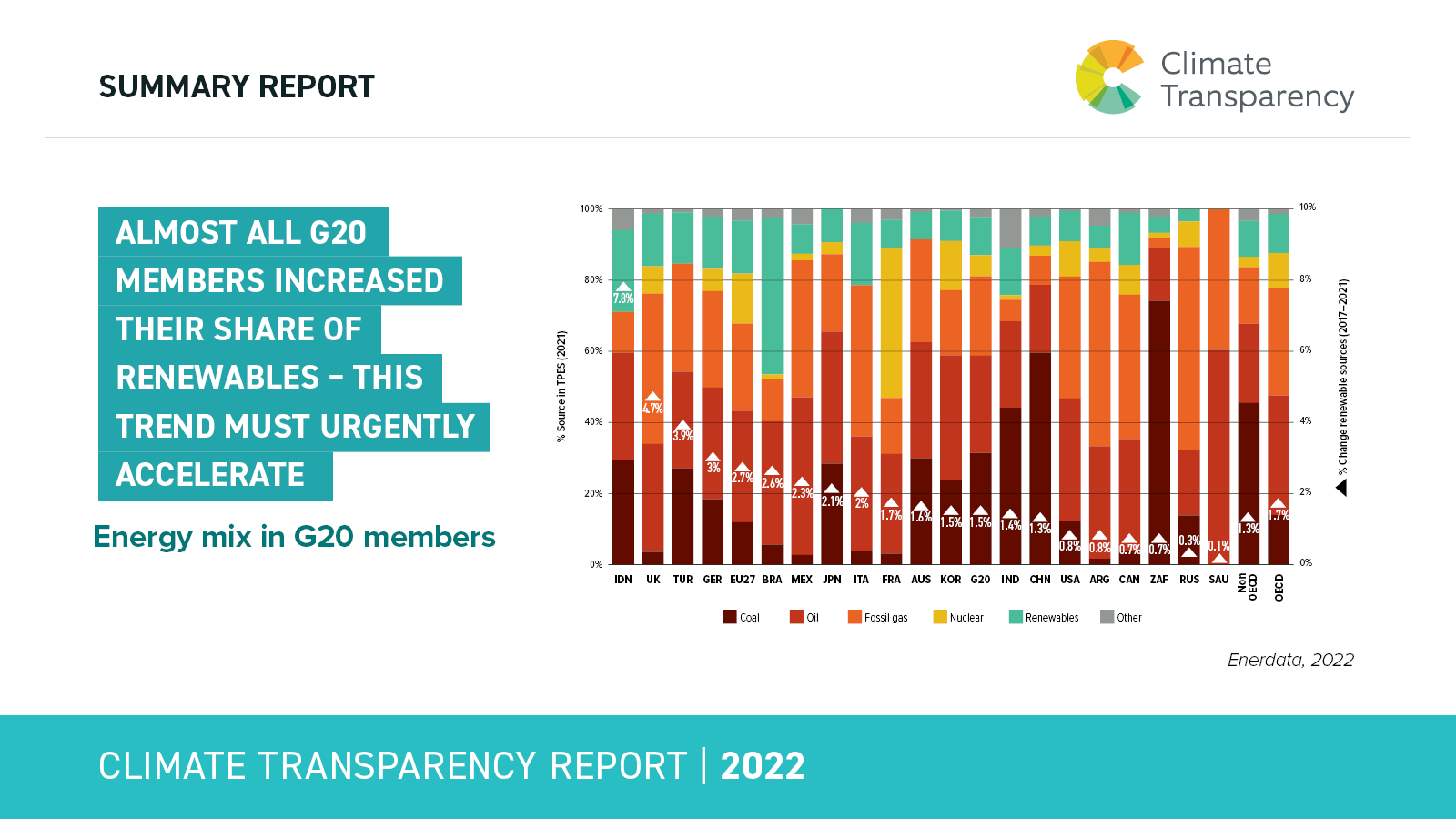

And, indeed, there are signs that the high road is getting more attractive. Our report indicates that the share of renewable energy in the energy mix has increased in almost all G20 countries – though not yet to the extent needed. For 2022, the IEA expects only a 1% increase in emissions globally, not least due to the expansion of renewable energy deployment all over the world.

In response to the skyrocketing energy prices in the past year, the value of energy has become more prominent – not only in monetary terms, but also in terms of the service it provides, and its necessity for modern living. As a consequence, measures to improve energy efficiency as well as energy sufficiency are gaining traction as a highway to reduce emissions and reign in energy prices.

It is still a hard choice to commit to the high road for many governments of the G20 – especially since the high price of gas also has made previously unattractive investments seemingly much more viable. The old and tired narrative of fossil gas as a bridge fuel is being told again sometimes as well, even though this has been thoroughly debunked.

The more attractive scenario is that the cost of new renewable energy installations has debunked where they can in almost all cases compete with electricity generation from fossil fuels. If harmful subsidies to the fossil fuel industry were finally phased out, the price signal in favour of renewable energy would only get stronger.

So, governments of the G20 really only have the option to follow the high road – both for monetary and moral reasons. Their decisions will be a critical signal for all other countries. If the G20 are not living up to their responsibility and showing active leadership – who should?